Miláčik čitateľov je práve vypredaný

Viac o knihe

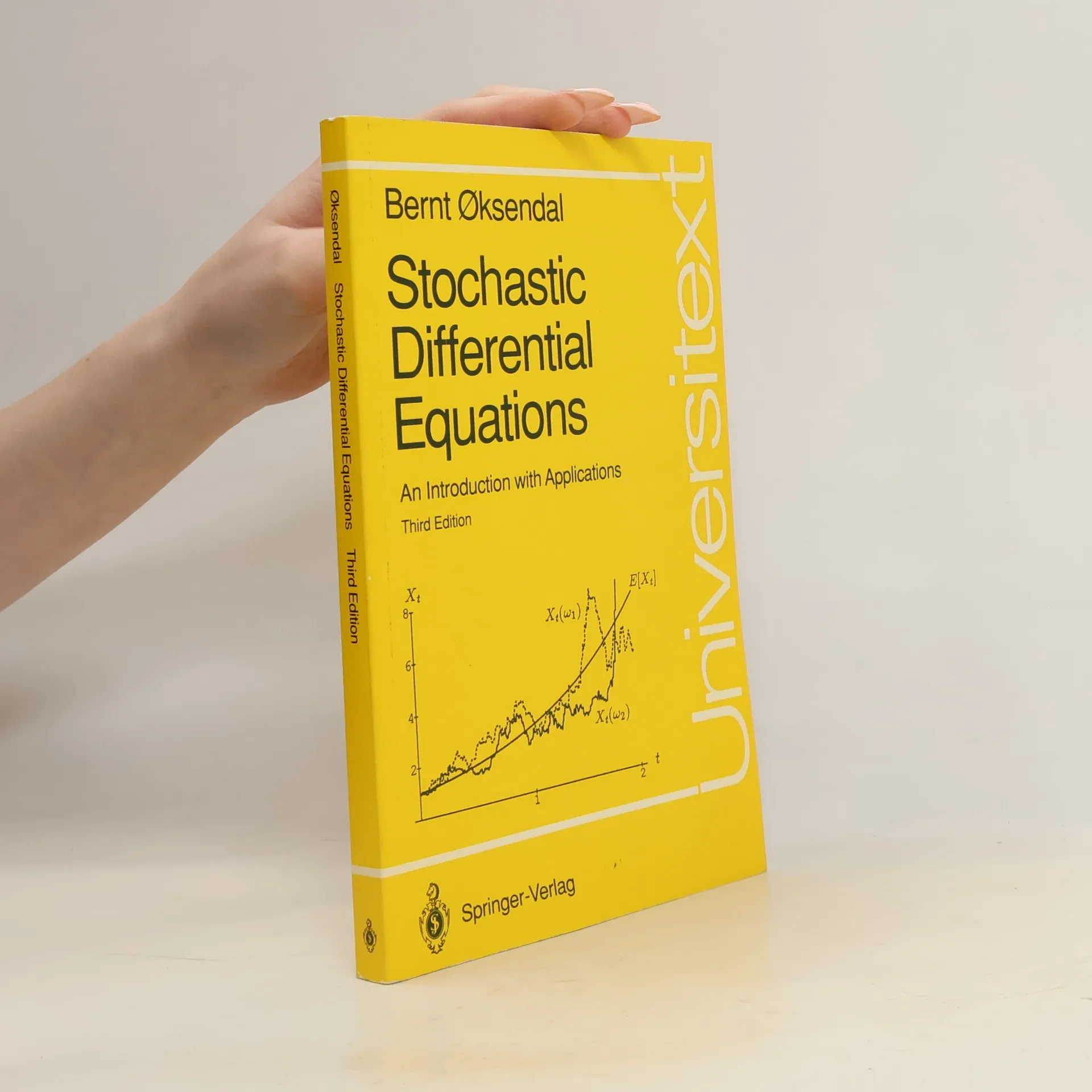

This book gives an introduction to the basic theory of stochastic calculus and its applications. Examples are provided throughout the text to motivate and illustrate the theory and show its importance for many applications in economics, biology, and physics. The basic idea of the presentation is to start from some fundamental results (without proofs) of the easier cases and develop the theory from there, concentrating on the proofs of the easier cases (which are often sufficiently general for many purposes) to quickly reach the parts of the theory that are most important for the applications. An extra chapter on applications to mathematical finance is included.

Nákup knihy

Stochastic Differential Equations, Bernt Oksendal

- Jazyk

- Rok vydania

- 1992

- product-detail.submit-box.info.binding

- (mäkká)

Akonáhle sa objaví, pošleme e-mail.

Platobné metódy

Tu nám chýba tvoja recenzia

- Titul

- Stochastic Differential Equations

- Podtitul

- An Introduction with Applications

- Jazyk

- anglicky

- Autori

- Bernt Oksendal

- Rok vydania

- 1992

- Väzba

- mäkká

- Počet strán

- 239

- ISBN10

- 3540533354

- ISBN13

- 9783540533351

- Série

- Štítky

- Náučná literatúra, Učebnice, Byznys, Biznis & Manažment, Prírodné vedy, Veda, Ekonómia, Učebnice matematiky, Financie, Učebnice fyziky

- Hodnotenie

- 4 z 5

- Anotácia

- This book gives an introduction to the basic theory of stochastic calculus and its applications. Examples are provided throughout the text to motivate and illustrate the theory and show its importance for many applications in economics, biology, and physics. The basic idea of the presentation is to start from some fundamental results (without proofs) of the easier cases and develop the theory from there, concentrating on the proofs of the easier cases (which are often sufficiently general for many purposes) to quickly reach the parts of the theory that are most important for the applications. An extra chapter on applications to mathematical finance is included.