Viac o knihe

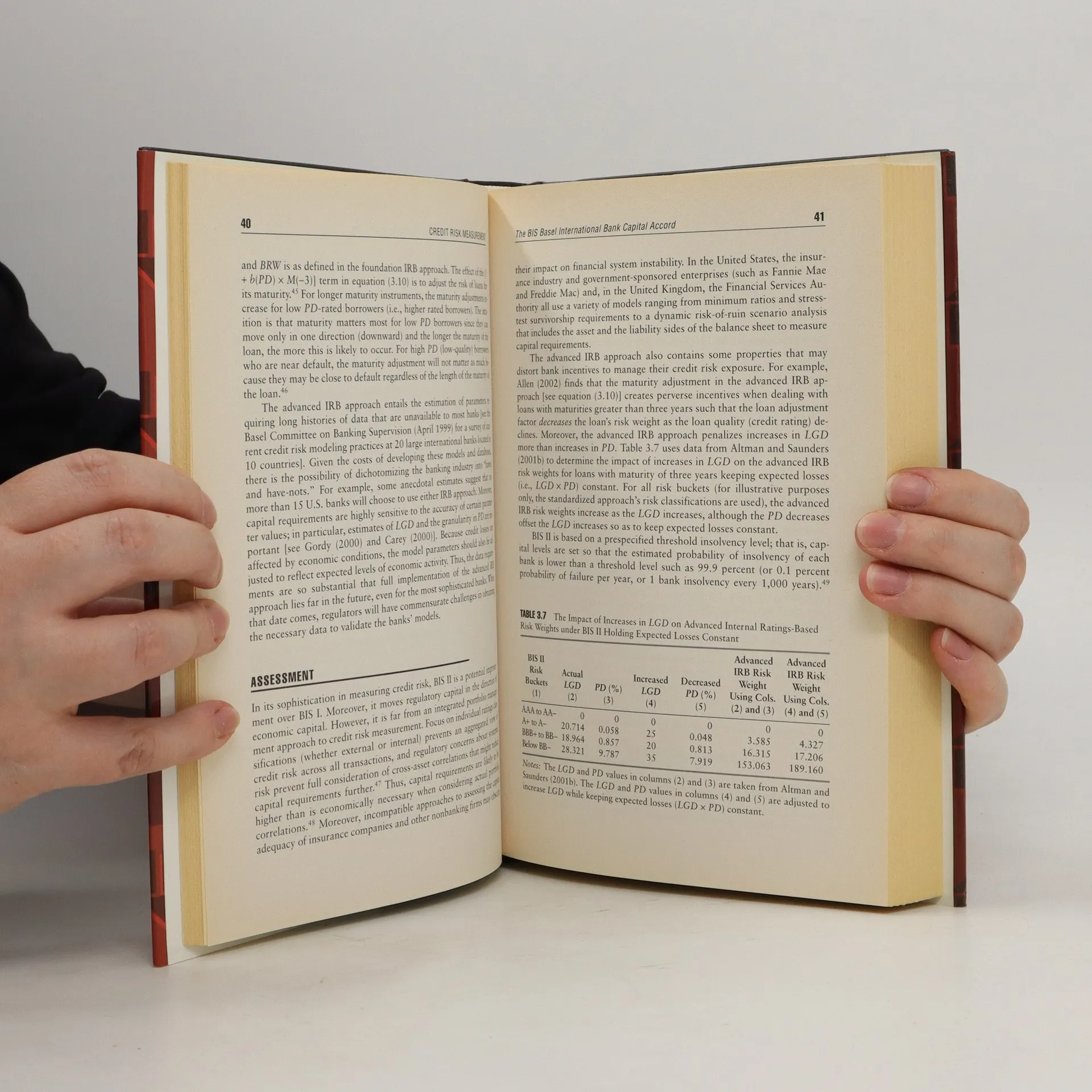

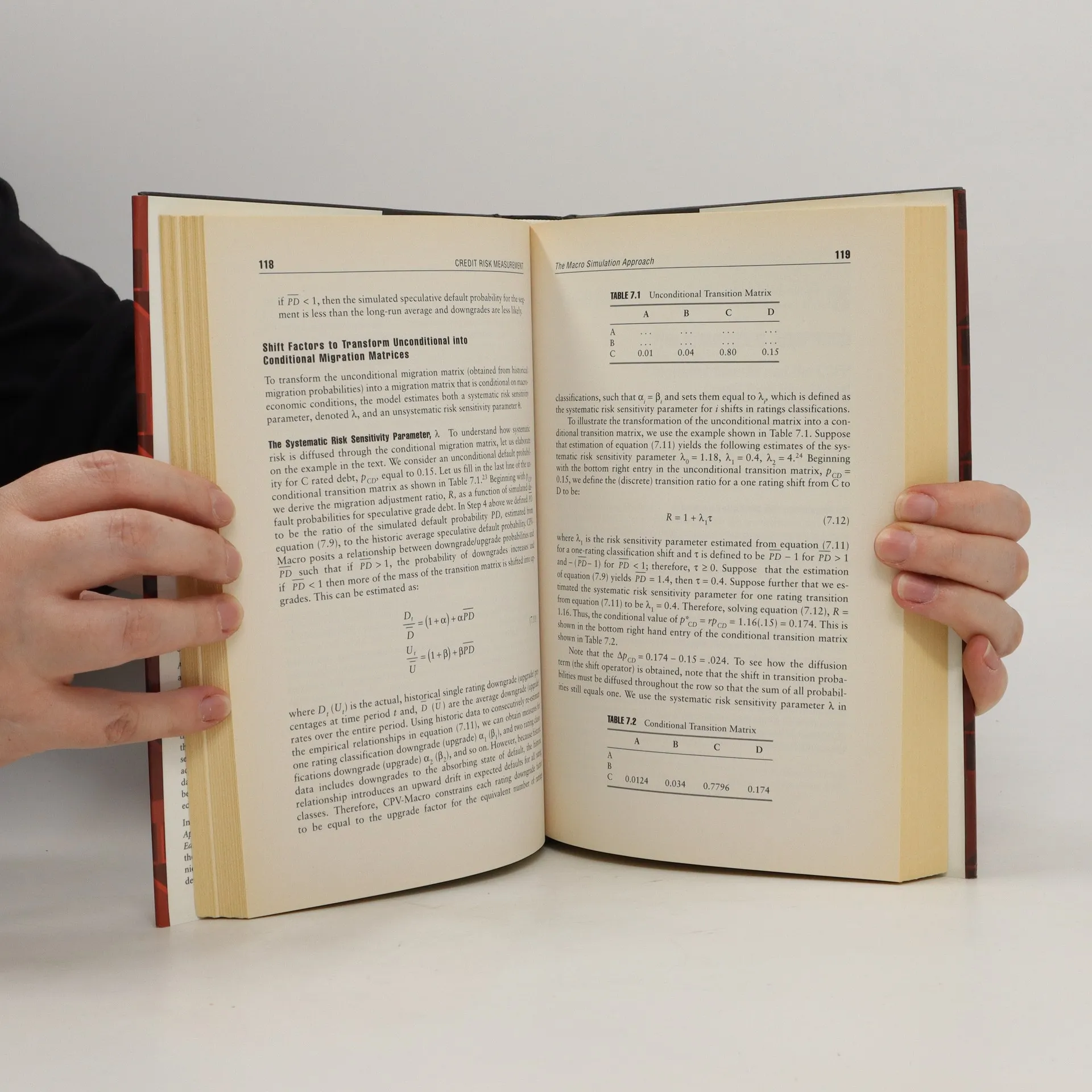

This comprehensive guide on credit risk measurement and management offers the latest insights into pricing and modeling techniques crucial for professionals in the financial sector. Since the early 1990s, the importance of understanding credit risk has surged, making this updated edition essential for credit risk professionals. The text covers alternative approaches to credit risk measurement, including new chapters on advanced models such as intensity-based models. It also addresses significant changes in banking regulations affecting credit risk practices at financial institutions. With its fresh perspectives and updated information, this work serves as a vital reference for those in the field. The authors, Anthony Saunders and Linda Allen, are esteemed academics with extensive experience in finance. Saunders is a professor at NYU's Stern School of Business and has held influential roles related to the Federal Reserve and various finance journals. Allen, a professor at Baruch College and adjunct at NYU, has authored notable works in finance. This book is part of the Wiley Finance series, renowned for providing essential knowledge and insights for financial professionals navigating the rapidly evolving landscape of financial markets and instruments.

Nákup knihy

Credit risk measurement : new approaches to value at risk and other paradigms, Anthony Saunders, Linda Allen

- Jazyk

- Rok vydania

- 2002

- product-detail.submit-box.info.binding

- (pevná)

Platobné metódy

Tu nám chýba tvoja recenzia

- Titul

- Credit risk measurement : new approaches to value at risk and other paradigms

- Jazyk

- anglicky

- Autori

- Anthony Saunders, Linda Allen

- Vydavateľ

- John Wiley & Sons

- Rok vydania

- 2002

- Väzba

- pevná

- Počet strán

- 336

- ISBN10

- 047121910x

- ISBN13

- 9780471219101

- Série

- Hodnotenie

- 3,6 z 5

- Anotácia

- This comprehensive guide on credit risk measurement and management offers the latest insights into pricing and modeling techniques crucial for professionals in the financial sector. Since the early 1990s, the importance of understanding credit risk has surged, making this updated edition essential for credit risk professionals. The text covers alternative approaches to credit risk measurement, including new chapters on advanced models such as intensity-based models. It also addresses significant changes in banking regulations affecting credit risk practices at financial institutions. With its fresh perspectives and updated information, this work serves as a vital reference for those in the field. The authors, Anthony Saunders and Linda Allen, are esteemed academics with extensive experience in finance. Saunders is a professor at NYU's Stern School of Business and has held influential roles related to the Federal Reserve and various finance journals. Allen, a professor at Baruch College and adjunct at NYU, has authored notable works in finance. This book is part of the Wiley Finance series, renowned for providing essential knowledge and insights for financial professionals navigating the rapidly evolving landscape of financial markets and instruments.