Viac o knihe

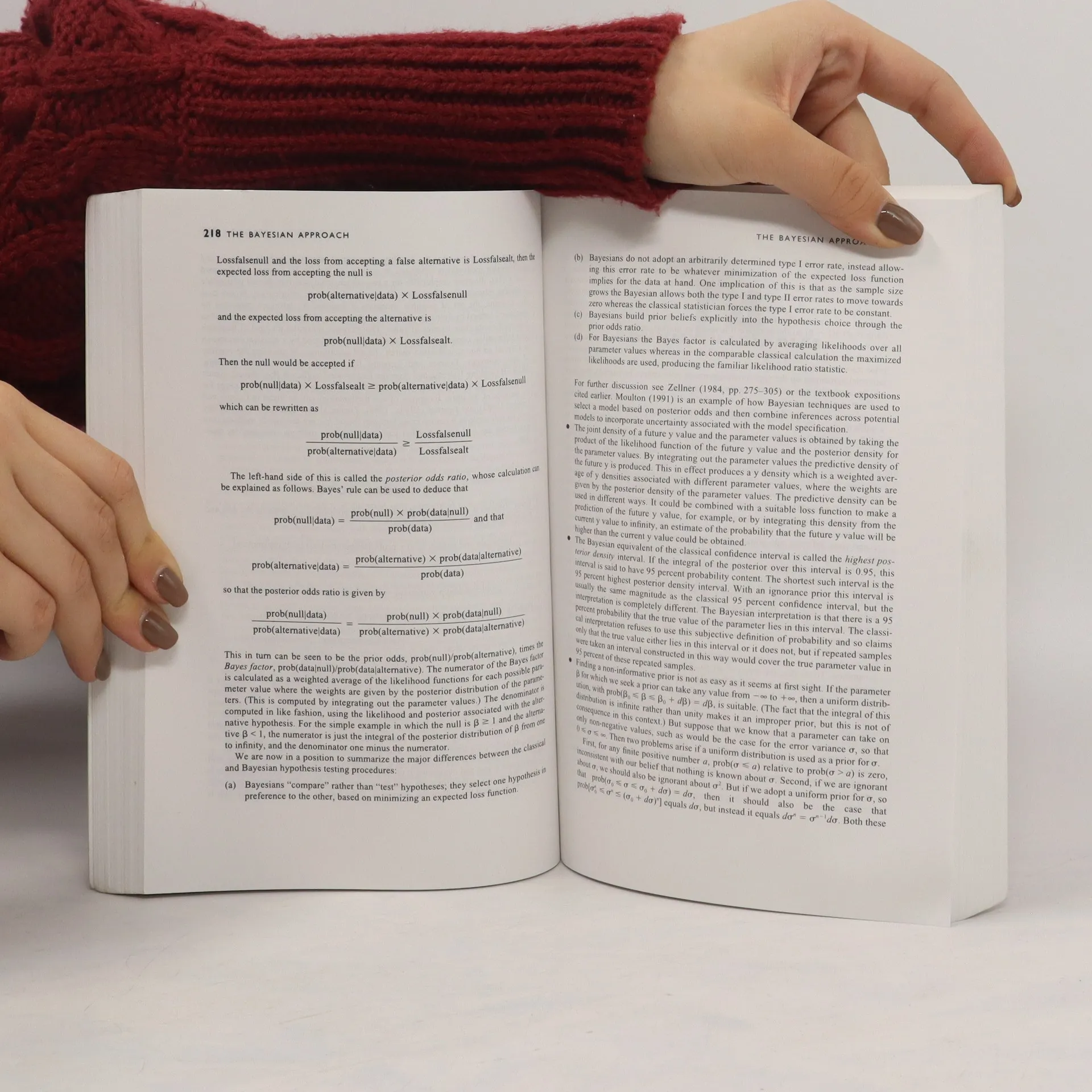

"Peter Kennedy's book, which provides intuitive, narrative explanations for a wide range of topics covered in undergraduate and graduate econometrics courses, occupies a unique position in the econometrics textbook market." -- David Ribar, Department of Economics, the George Washington University "A Guide to Econometrics" has established itself as the first-choice text for teachers and students throughout the world. It provides an overview of the subject and an intuitive feel for its concepts and techniques without the notation and technical detail often characteristic of econometrics textbooks. The fourth edition updates the contents and references thoughout, while retaining the basic structure and flavor of earlier editions. New material has been added on several topics, such as bootstrapping, count data, duration models, generalized method of moments, instrumental variable estimation, linear structural relations, Monte Carlo studies, neural nets, time series analysis, and VARs. A new appendix and a new type of exercise underline the importance of the sampling distribution concept.

Nákup knihy

A guide to Econometrics, Peter Kennedy

- Jazyk

- Rok vydania

- 1998

- product-detail.submit-box.info.binding

- (mäkká)

Platobné metódy

Tu nám chýba tvoja recenzia

- Jazyk

- anglicky

- Autori

- Peter Kennedy

- Vydavateľ

- MIT Press

- Rok vydania

- 1998

- Väzba

- mäkká

- ISBN10

- 0262611406

- ISBN13

- 9780262611404

- Série

- Štítky

- Náučná literatúra, Učebnice, Byznys, Biznis & Manažment, Ekonómia, Učebnice matematiky, Financie

- Hodnotenie

- 4,25 z 5

- Anotácia

- "Peter Kennedy's book, which provides intuitive, narrative explanations for a wide range of topics covered in undergraduate and graduate econometrics courses, occupies a unique position in the econometrics textbook market." -- David Ribar, Department of Economics, the George Washington University "A Guide to Econometrics" has established itself as the first-choice text for teachers and students throughout the world. It provides an overview of the subject and an intuitive feel for its concepts and techniques without the notation and technical detail often characteristic of econometrics textbooks. The fourth edition updates the contents and references thoughout, while retaining the basic structure and flavor of earlier editions. New material has been added on several topics, such as bootstrapping, count data, duration models, generalized method of moments, instrumental variable estimation, linear structural relations, Monte Carlo studies, neural nets, time series analysis, and VARs. A new appendix and a new type of exercise underline the importance of the sampling distribution concept.